What is the 13th-month pay law? Learn all about this mandated benefit, including its coverage and exemptions.

Key Points

- The 13th-month pay is a mandatory salary for all rank-and-file employees in the Philippines.

- It is equal to the total basic annual salary earned by the employee during the year divided by the number of months they have worked.

- In general, employers must release this pay before December 15 of each year.

The thirteenth-month pay is a mandatory benefit for private employees in the Philippines, regardless of employment status. Below are the 13th month pay rules and computation guide.

What is the 13th-month pay?

The 13th-month pay is a mandatory form of compensation in the Philippines secured by Presidential Decree No. 851. Rank-and-file employees receive this benefit, which serves as an important financial assistance at the end of the year.

13th-month pay computation Philippines

To determine the 13th-month pay, you only need the employee’s total basic salary. Here’s how to compute your 13th month pay:

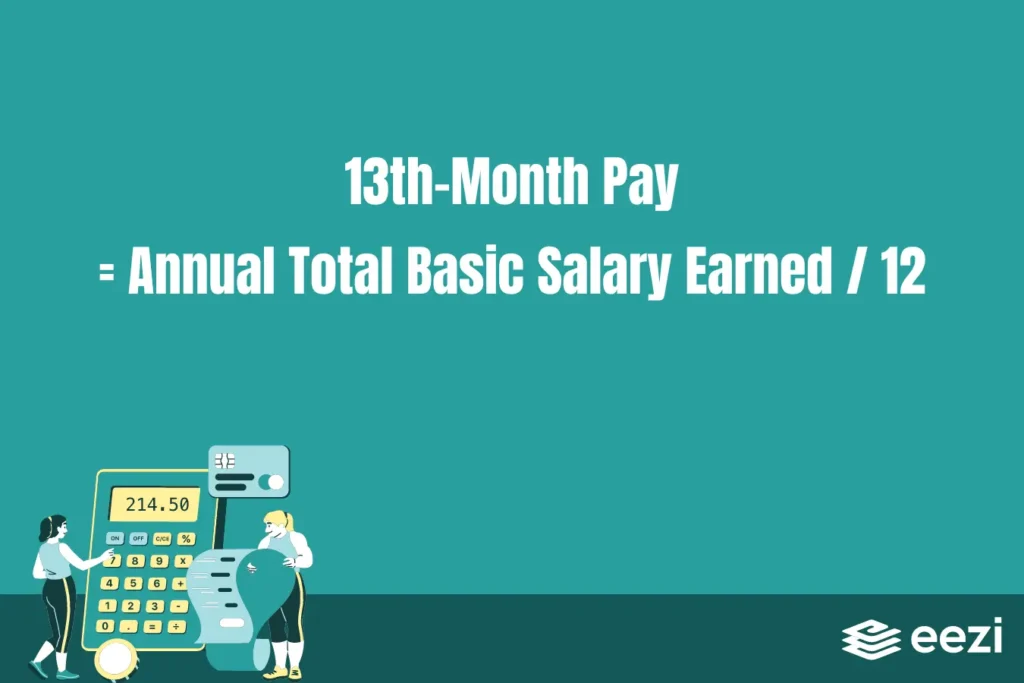

The formula for computing the 13th-month pay is:

13th-Month Pay = Annual Total Basic Salary Earned / 12

Example 1: An employee worked the entire year.

An employee (Joe) has a basic monthly salary of Php 16,500. If Joe worked for the entire year and had no absences or deductions, he would receive Php 16,500 as his 13th-month pay.

(Basic Salary x 12 months) / 12

(Php 16,500 x 12 – Php 7,643) / 12

= Php 16,500

Example 2: An employee has absences within the calendar year.

For instance, Joe has incurred a total of Php 7,643.00 worth of deductions from absences. In this case, his 13th-month pay computation is:

(Basic Salary x 12 – Deductions ) / 12

(Php 16,500 x 12 – Php 7,643) / 12

Php 198,000 – Php 7,643 = Php 190,357 / 12

= Php 15,863

Joe’s total basic salary for the year, minus the deductions, is Php 190,357.00. Next, we divide Php 190,357 by 12 and get Php 15,863.

Example 3: An employee has worked for less than a year.

An employee who has worked for less than a year will still receive a pro-rated 13th-month pay.

To compute pro-rated pay, you will need the employee’s basic salary. The formula for the pro-rated 13th-month pay is as follows:

(Monthly Basic salary x Number of Months Worked – Total Deductions) / 12 = Pro-Rated 13th-Month Pay

For example, Joe has only worked from September to December, and his basic monthly salary is Php 15,000. If Joe has no deduction for the entirety of this period, his pro-rated 13th-month pay can be computed as:

(Php 15,000 x 4) / 12

Php 60,000 / 12

= Php 5,000

Suppose Joe has unpaid absences with deductions amounting to Php 6,480.50. In this case, we can compute his pro-rated 13th-month pay as:

(Php 15,000 x 4 – Php 6,480.50) / 12

(Php 60,000 – Php 6,480.50) / 12

53, 519.50 / 12

= Php 4,459.96

The total basic salary or annual salary does not include unpaid absences, overtime pay, holiday pay, night shift differential, and allowances. Moreover, it does not include monetary benefits such as the cash equivalent of unused vacation and sick leave credits.

What earnings are not included in the computation?

The 13th-month calculation Philippines excludes certain earnings and allowances. Among the excluded earnings are:

- Overtime Pay

- Holiday Pay

- Night Shift Differential

- Bonuses and Incentives

- Commissions

- Profit Sharing

- Allowances

eezi HR Guide

Learn how to make a simple yet compliant pay slip for your employees.

DOLE Rules on 13th-month pay

Mandated by law

- 13th-month pay is a government-mandated employee benefit that rank-and-file employees are entitled to receive

- This legal mandate ensures that eligible employees receive this additional compensation.

13th month pay release deadline

- The law specifies that the 13th-month pay must be paid not later than December 24 each year.

- Some employers choose to provide this benefit in two releases, with half given around mid-year and the other half in December.

The 13th-month pay law

Under the Labor Code, the 13th-month pay is mandatory for employers in the Philippines. Moreover, DOLE requires employers to submit their compliance reports on or before January 15 of every year.

Moreover, the law provides the following:

- A mandatory benefit: The 13th-month pay law mandates that all employers in the Philippines must grant their employees this pay before December 25 each year.

- It must be 1/12th of the annual basic salary: The law initially applied to employees earning up to Php 1,000 per month, entitling them to receive one-twelfth (1/12) of their basic salary for the entire calendar year. In 1986, former President Corazon Aquino signed a memorandum that removed the salary ceiling, making rank-and-file employees of all income levels eligible to receive the 13th-month bonus.

- It is not taxable if it is less than or equal to Php 90,000: The TRAIN law raised the tax exemption ceiling for the 13th-month pay from Php 82,000 to Php 90,000, benefiting a broader range of employees.

eezi HR Guide

Stay compliant with the required employee benefits in the Philippines.

FAQs

General rules

Who is eligible for 13th month pay?

Under the Department of Labor and Employment’s (DOLE) guidelines, the following private-sector employees should receive their 13th-month pay:

- Rank-and-file employees who have worked in the company for at least a month within the calendar year.

- Contractual employees

- Relievers

- Seasonal workers

- Discharged or terminated employees as part of their back pay (those who resigned before the issue of the 13th-month pay)

- Employees with multiple employers

- Terminated employees

- Employees on maternity leave

However, those who have worked for less than a year in the company will only receive a pro-rated 13th month bonus. Moreover, the months where an employee was out due to maternity leave shall not be part of the 13th-month’s computation. In other words, the pay will be based solely on the number of months of their employment with the company.

Who is not guaranteed a 13th-month pay?

- Government employees, including those hired by government-owned and controlled corporations

- Managerial employees (unless stipulated in their employment contract)

When to give 13th month pay?

The 13th month pay is required to be made on or before December 24 of every year. Some companies prefer to pay employees twice a year (in June and December), although the majority choose to do so at the end of the year.

Do government employees receive 13th-month pay?

Unlike private employees, government employees are not guaranteed to receive 13th-month pay under the law. However, they may still receive other bonuses that equals the amount of a 13th-month pay. for instance, they may receive mid-year bonuses at around June to July.

It’s already December 25, and I haven’t received my 13th-month pay yet. What should I do?

If you think your employer really has no intention of releasing your 13th-month pay, you may contact DOLE through their hotlines or fill out their online query form. Not giving employees their 13th-month benefit on or before December 24 is punishable by the law.

Inclusions

Are monetary benefits included in the 13th-month pay computation?

Unless it is in the employee’s Collective Bargaining Agreement (CBA), allowances and other monetary benefits are not part of the computation. In other words, the computation will only factor the basic pay.

Other monetary benefits that are not part of this pay computation are:

Is overtime included in 13th month pay?

No, overtime pay is not included in the 13th Month Pay computation. The computation is based on the basic salary of an employee.

Is the 13th-month pay the same as the Christmas bonus?

No, the 13th-month pay and the Christmas bonus are not the same. The 13th-month pay is a mandatory benefit in the Philippines that employers must give before December 25 of each year. Moreover, failing to do so can subject employers to legal consequences for non-compliance.

In contrast, Christmas bonuses is not mandatory for employers under Philippine Law. Often, this is a voluntary benefit employers offer during the holiday season as a goodwill gesture. Unlike the 13th-month pay, there is no law that requires employers to provide Christmas bonuses.

How to compute Christmas bonus?

The Christmas bonus computation varies, and it is not the same as the 13th month’s pay. It can be a fixed amount, a percentage of income, or based on company performance or other factors.

Is 13th-month pay taxable in the Philippines?

No. The 13th-month pay is typically exempt from taxes as long as it does not exceed Php 90,000. Before the TRAIN Law, the tax ceiling was Php 82,000.

Eligibility

What happens if I resign or get terminated before the release of the 13th-month credit?

As per the rules for 13th month pay for resigned employee, those who are eligible for the 13th-month benefit are still entitled to receive them even if they are separated from work due to resignation or termination. As long as the private employee has worked for at least one month, they are entitled to receive the 13th-month credit.

If I get separated from work, when can I get my 13th-month credit?

Eligible employees who have been separated from work usually receive their 13th-month credit along with their final or back pay. It might take some time before it is released after the resignation has been filed.

13th-Month Pay Exemptions

Although the 13th-month salary is mandatory by law, some companies or agencies are exempt from paying it to their employees.

Government

This includes all departments, agencies, and any political subdivision. It also includes all government-owned and controlled corporations that do not operate as private subsidiaries of the government.

Household Workers’ Employers

The employers of household helpers and persons in the personal service of another relating to such workers are also exempt from paying the 13th-month benefit.

Employers paying by commission, boundary, or task

Employers who pay based solely on commission, boundary, or task basis and those who pay a fixed or guaranteed wage for the performance of a specific task, regardless of the hours consumed in the performance of said task, are exempt from paying the 13th month.

13th Month Pay Report

Employers who are required to issue a 13th-month pay must also submit their compliance report. Moreover, submission of this report must not be later than January 15 of the following year. Lastly, this report must also include the following information:

- Establishment name

- Product or business

- Total Employment

- Total Workers

- Amount of Benefits Granted

Always credit 13th-month benefits on time

Enroll your company in an automated payroll for accurate and timely 13th-month benefit credit.